What Is the 50 30 20 Rule?

The 50 30 20 rule is a popular budgeting strategy that organizes your monthly salary into three percentage-based categories, making it easier to manage expenses and savings.

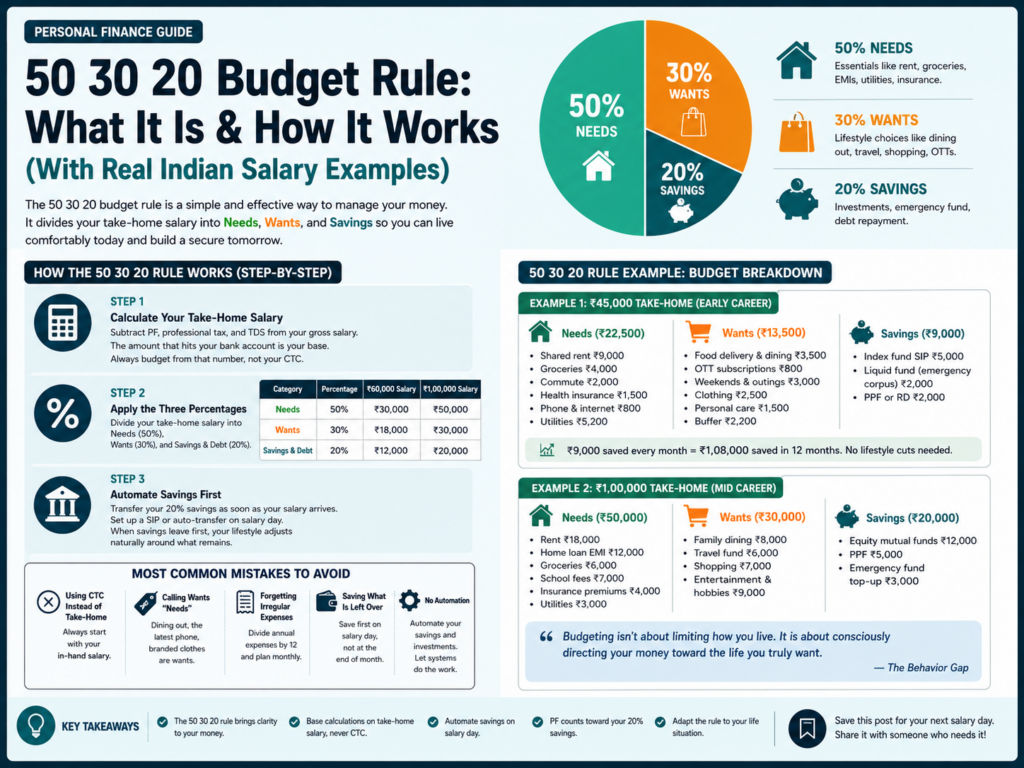

The Three Categories

50% for Needs

Rent, groceries, EMIs, utilities, insurance

30% for Wants

Dining out, OTT subscriptions, travel, shopping

20% for Savings and debt repayment

SIPs, PPF, emergency fund, credit card dues

It was introduced by US Senator Elizabeth Warren in her book All Your Worth (2005).

The entire framework runs on your in-hand salary, not your CTC.

“The secret to financial security is not how much you earn. It is building a system that works regardless of the number.”

— All Your Worth

How Does the 50 30 20 Rule Work? (Step-by-Step)

Step 1: Calculate Your Take-Home Salary

To determine your take-home salary, subtract PF, professional tax, and TDS from your gross monthly income.

The number that hits your bank account is your base.

For a ₹60,000 CTC package, your in-hand might be closer to ₹48,000–₹52,000.

Always budget from that number.

Step 2: Apply the Three Percentages

| Category | Percentage | ₹60,000 Salary | ₹1,00,000 Salary |

| Needs | 50% | ₹30,000 | ₹50,000 |

| Wants | 30% | ₹18,000 | ₹30,000 |

| Savings & Debt | 20% | ₹12,000 | ₹20,000 |

Step 3: Automate Savings First

Transfer your 20% savings the moment your salary arrives, before you touch anything else.

Set up a SIP or auto-transfer on salary day.

When savings leave first, your lifestyle naturally adjusts around what remains.

50 30 20 Rule Example: Budget Breakdown for Two Indian Salaries

Example 1: ₹45,000 Take-Home (Early Career)

Needs (₹22,500)

Shared rent ₹9,000

Groceries ₹4,000

Commute ₹2,000

Health insurance ₹1,500

Phone and internet ₹800

Utilities ₹5,200

Wants (₹13,500)

Food delivery and dining ₹3,500

OTT subscriptions ₹800

Weekends and outings ₹3,000

Clothing ₹2,500

Personal care ₹1,500

Buffer ₹2,200

Savings (₹9,000)

Index fund SIP ₹5,000

Liquid fund (emergency corpus) ₹2,000

PPF or RD ₹2,000

₹9,000 saved every month equals ₹1,08,000 saved in 12 months.

No lifestyle cuts needed.

Example 2: ₹1,00,000 Take-Home (Mid Career)

Needs (₹50,000)

Rent ₹18,000

Home loan EMI ₹12,000

Groceries ₹6,000

School fees ₹7,000

Insurance premiums ₹4,000

Utilities ₹3,000

Wants (₹30,000)

Family dining ₹8,000

Travel fund ₹6,000

Shopping ₹7,000

Entertainment and hobbies ₹9,000

Savings (₹20,000)

Equity mutual funds ₹12,000

PPF ₹5,000

Emergency fund top-up ₹3,000

Budgeting isn’t about limiting how you live. It is about consciously directing your money toward the life you truly want.

— The Behavior Gap

50 30 20 Rule for Beginners: Every Question Answered

What Counts as a Need vs a Want?

A need is something that breaks your daily life if removed.

Rent, food, electricity, transport to work, medication.

A want improves your comfort or enjoyment but is a choice, not a requirement.

The line blurs sometimes. A gym membership is a need if it manages a health condition.

It is a want if you just prefer it to free alternatives.

The rule does not judge. It asks you to be honest.

Is the 50 30 20 Budget Rule Good for Indian Salaries?

Yes, with one adjustment.

In cities like Mumbai or Bangalore, rent alone can consume 30–40% of a lower income.

On a ₹35,000 salary with ₹12,000 rent, you are already at 34% before food, commute, or utilities.

A 2023 BankBazaar survey found only 27% of Indian millennials had a structured savings habit.

If your needs genuinely exceed 50%, move to 60/20/20 temporarily.

Protect the savings bucket above everything else.

Where Do EMIs Fit?

Home loan and vehicle EMIs go under Needs because they fund essential assets.

Personal loan EMIs and credit card dues go under the 20% bucket as debt repayment.

Paying down high-interest debt builds net worth just as effectively as investing.

Most Common Mistakes With the 50 30 20 Budgeting Rule

Using CTC Instead of Take-Home

Your CTC is a hiring number.

Your in-hand salary is your budgeting number.

If your CTC is ₹8 LPA but your in-hand is ₹52,000, every calculation must start from ₹52,000.

Calling Wants “Needs” to Justify Them

Dining out daily, the latest phone, branded clothing are wants.

Labelling them needs does not change what they are.

It just silently eats your savings.

Forgetting Irregular Expenses

Annual premiums, festival shopping, travel, quarterly subscriptions should be divided by 12 and included monthly.

Surprise expenses are only surprising when ignored in planning.

Saving What Is Left Over

Saving at month-end almost never works.

Pay yourself first on salary day.

Set up your finances on autopilot so smart money choices happen automatically without relying on self-control.

When to Adjust the 50 30 20 Rule

The 50 30 20 rule is a starting framework, not a permanent fixed rule.

| Life Situation | Suggested Split |

| High rent city, early career | 60 / 20 / 20 |

| Aggressive debt payoff phase | 50 / 10 / 40 |

| High income, low fixed costs | 40 / 20 / 40 |

| Single income, supporting family | 65 / 15 / 20 |

One insight most Indian guides miss:

Your employer’s PF deduction already counts toward your 20% savings.

If ₹3,600 leaves your salary as PF every month, your voluntary savings target is already partially met.

Key Takeaways

- The 50 30 20 budget rule splits take-home income into Needs (50%), Wants (30%), Savings (20%)

- Always base calculations on in-hand salary, never CTC

- Automate savings on salary day

- PF deductions count toward your 20%

- Adjust the split based on life stage

- Paying off high-interest debt is saving

The 50 30 20 budgeting rule works because it is simple enough to actually use.

You do not need a perfect financial situation to start.

You just need your salary figure and three calculations.

Try it for 60 days and watch how quickly clarity replaces anxiety.